Banks Could Rival Big Techs Again

Banks may be able to catch up with big technology firms in terms of client acquisition as the latter group loses customer «float» and face tighter financial regulations. Some believe the era of big payment giants is going.

Over the last decade, big technology firms (Big Techs) and fintechs have flourished on keeping customer «float» and earning interest on it, just like banks. Except, they are not regulated like banks. However, the landscape is starting to change, especially in China.

Two years ago, People's Bank of China (PBoC) announced that it required third party payment groups to keep 20 percent of customers in a single dedicated non-interest-bearing custodial account at a commercial bank. This was then increased to 50 percent in April 2017.

By January this year, the amount is increased to 100 percent. This practically cuts off Big Techs’ ability to rehypothecate (ie. post funds as collateral at banks to gain a fee or discount on sevices), or use these funds for lending activities.

Ability to Arbitrage

Agustín Carstens of the Bank of International Settlements (BIS) distinguishes fintechs with big tech companies: «Fintechs offer financial services with digital technology whereas big tech firms offer technology services as their primary business,» he said in a keynote address at the recent «FT Banking Summit». In particular, the latter’s advantage lies in the exploitation of existing customer networks and the massive quantities of data generated by their business lines.

Big Techs and certain fintechs have been able to benefit from their ability to arbitrage interest-rate differentials due to the uneven regulatory fields. They typically pay their customers zero interest and then they collect interest from banks where they park their float.

Played On Uneven Fields

Some Big Techs could also use their customers’ float to offer money market funds, such as Yu’e bao via Ant Financial, financial products, or extend credit facilities, but without the usual regulations imposed on them. Even though banking chiefs have decried the unfairness, regulators have been slow to impose capital requirements on Big Techs for fear of stifling their local tech companies.

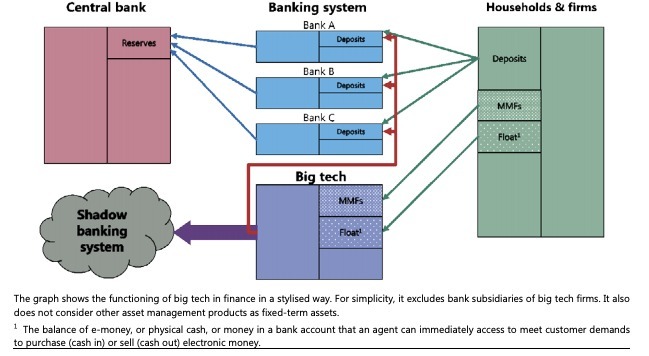

Just as money market funds can pose systemic risks, Big Techs could also be subject to investor runs in the event of credit or duration losses. In a similar light, if big tech deposit customer funds directly with banks, they create a parallel payments system that is not properly overseen by the central bank, Agustín Carstens said. «This could potentially undermine financial stability and shield payments from the scrutiny of authorities guarding against illegal activities, such as money laundering,» he said (see graphic below).

Big Tech in China

(Source: Agustín Carstens speech)

- Page 1 of 2

- Next >>