When the Brakes Fail: UBS and the Collapse of First Brands

It is the biggest US corporate default in years — and, so far, only one global bank is caught in its wake. finews.asia reveals how UBS Asset Management promoted its working-capital funds to professional investors, marketing that now sits uneasily beside the bank’s outsized exposure to the collapse of First Brands Group.

When First Brands Group filed for Chapter 11 protection on 29 September 2025, in the US Bankruptcy Court for the Southern District of Texas, it disclosed more than $10 billion in liabilities against roughly $3.5 billion of annual revenue.

The once-profitable manufacturer and distributor of automotive aftermarket components – filters, braking systems, wipers and related replacement parts – had transformed into a web of layered financing vehicles and circular cash flows.

A Capital-Structure Experiment

What began as an ordinary parts supplier evolved into a capital-structure experiment: receivables were factored through multiple originators, inventory collateral allegedly commingled or pledged to several lenders, and billions in payables securitized off-balance sheet.

By the time liquidity vanished, even its own creditors struggled to determine what counted as real collateral.

UBS Stands Out

Among the wreckage, one name stands out. The UBS Hedge Fund Solutions platform and UBS O’Connor funds together emerged as First Brands’ largest unsecured financial creditors, with $349.8 million in supply-chain-finance claims and additional secured exposures that push the total above $500 million.

No other major bank appears on the list of unsecured creditors, although indirect involvement through the financing of working-capital originators or conduits could still emerge as the proceedings unfold.

Poorly Understood Risks?

The UBS revelation, first reported by «Bloomberg», came as a shock: As things stand, the case leaves a small player in US corporate finance standing out in an uncomfortable way. Among the world’s major banks, only UBS is visibly entangled in the collapse of First Brands.

While the direct impact on shareholders appears limited – the exposures sit in investment funds rather than on the UBS balance sheet – the episode nevertheless echoes earlier controversies. Just as with the complex dollar-linked derivatives sold to Swiss private wealth management clients, the bank may soon again find itself accused of promoting products whose risks were poorly understood, and whose marketing relied on arguments that now look questionable.

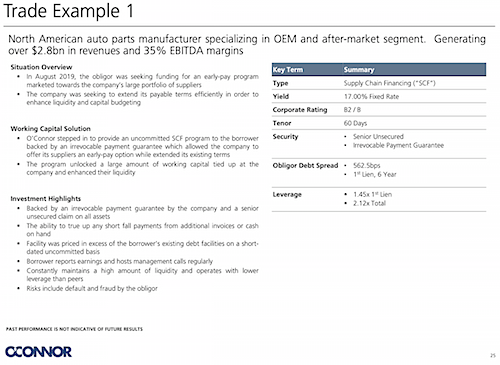

«Trade Example 1»: First Brands

In January 2023 – well after the Greensill disaster that helped sink Credit Suisse – UBS Asset Management distributed a 15-page investor deck titled «UBS Working Capital Finance Strategy.» The presentation, exclusively obtained by finews.asia, marketed the strategy to professional investors as a «short-duration, self-liquidating structure with greater yield, lower default, and higher recovery than comparable assets,» an opportunity promising double-digit returns.

On slide 25 («Trade Example 1»), the deck showcases a North American auto-parts manufacturer active in OEM and aftermarket, citing over $2.8 billion in revenue and a 35 percent EBITDA margin. It describes an uncommitted supply-chain-finance program begun in August 2019 to extend payables, with a fixed yield of 17 percent, 60-day tenor, and a B2 / B corporate rating.

UBS O'Connor: First Brands Group as «Trade Example 1» in January 2023. (Screenshot: finews.com; click to enlarge)

Startling Economics

The implied economics are startling. No soundly managed industrial company would willingly surrender 17 percent of its margin merely to shrink supplier payments for two months. In First Brands’ case, the rationale lay in an aggressive, debt-fuelled acquisition spree that left the balance sheet perpetually short of cash.

For credit investors, such pricing should have been a warning sign rather than an attraction — a textbook example of adverse selection, where the borrowers most willing to pay double-digit yields are not the most likely to survive them.

- Page 1 of 2

- Next >>

{kind=link}