finews.asia Releases Private Banking AUM League Table

In 2021, the biggest private banks in the storied high-growth region of Asia experienced a rare occurrence: total assets under management slipped lower. finews.asia takes stock of a historic year with the release of its 2021 AUM League Table.

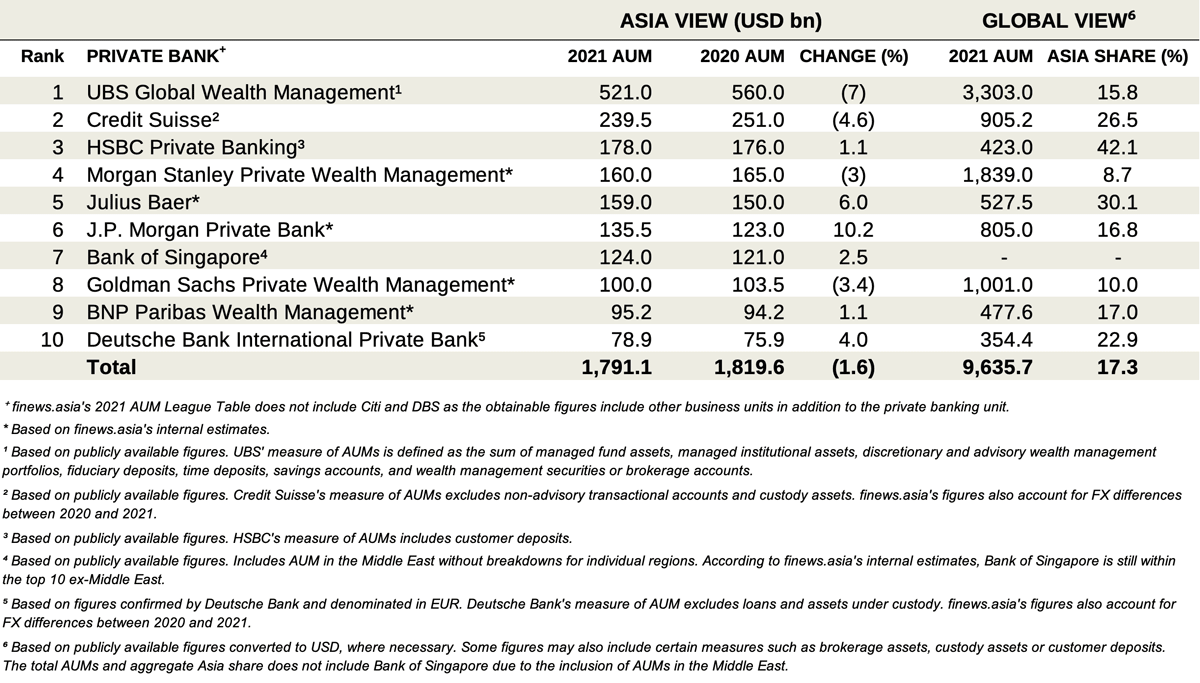

According to finews.asia’s 2021 AUM League Table, the top 10 private banks in Asia registered a total of $1.79 trillion in assets under management (AUM) as of the end of December last year, down 1.6 percent from $1.82 trillion in 2020.

This is an unprecedented event.

Marketwide de-risking by clients erased existing AUMs. Covid-linked disruptions impacted asset acquisition and slowed down client decision-making. Political uncertainty resulted in lasting changes in the behavior of certain client segments.

An Even Poorer Outlook

Poor market performance, most notably in China’s tech and real estate sector, is not sufficient to explain the uncharacteristic drop as the region has previously demonstrated that a bad year – or two – doesn’t deter AUM growth.

Chinese equities suffered even more severe turbulence in 2015 after the Shanghai Composite Index nearly halved from its peak level and followed up with the circuit breaker failure that saw the index lose another quarter in early 2016. In those same two years, 2021’s top 10 private banks in Asia posted 8.7 and 6.3 percent AUM growth, respectively, according to finews.asia data.

Poor sentiment and an even poorer outlook are the culprits as clients are not only retreating on their own but banks are also actively discouraging them from adding risk to portfolios.

Credit Suisse, for example, said in its latest first-quarter results that it has been undergoing a de-risking exercise in its wealth business since April 2021, underlining notable concentration risk in Asia where it reported a 1.1 percent AUM decrease to 218.8 billion Swiss francs ($239.5 billion) and a net outflow of 1.1 billion francs in 2021. Although Swiss rival UBS outdid itself in net new money ($26.4 billion, up from $25 billion in 2020), this was not enough to offset a $39 billion plunge in invested assets to $521 billion.

No Rising Tide For All

Traditionally both beneficiaries of strong growth and relative stability, the dual hubs of Asia did not have the same experience in 2021.

Hong Kong was hit with a double whammy of continued political uncertainty and tightening Covid-related restrictions. Meanwhile, Singapore maintained the status quo while steadily reopening for travel and business. Private banks with a strong presence in the latter and no excessive reliance on the former fared especially well.

The private banking arm of Deutsche Bank – whose Asia CEO Alexander von zur Muehlen sits in Singapore instead of Hong Kong where its predecessor resided – was the top growth leader amongst the pack with a 13 percent increase in Asia AUMs on a constant currency basis to 69.7 billion euros ($78.9 billion).

A noteworthy growth driver has been the emergence of Singapore-based China bankers which became increasingly in demand in the wake of the Hong Kong protests in 2019. J.P. Morgan Private Bank, for example, established China coverage out of Singapore in the same year and said it would double the team's size in late 2020 with an eye on capturing wealth linked to Chinese corporates setting up their international headquarter in the city-state. The American private bank’s Asia AUMs grew 10.2 percent to $135.5 billion in 2021.

Onshore Opportunity

And for private banks that extended beyond Asia's traditional hubs to directly reach clients in onshore markets – and help them avoid cross-border troubles – there were even more diversification benefits to be felt last year.

Julius Baer epitomized this best with a multi-pronged onshore strategy for various markets throughout the region, which was a key contributor to its 6 percent increase in AUMs to $159 billion in 2021.

The Swiss pure-play private bank has a tie-up in mainland China with the Beijing International Wealth Management Institute, a strategic partnership with Nomura in Japan and an onshore unit in India to complement its global coverage of non-resident Indians. In late 2020, it unveiled ambitions for its joint venture with Siam Commercial Bank to capture an estimated 10 percent of the Thai market of wealthy individuals with at least 100 million baht ($2.9 million) in investable assets or around $30 billion at the time.

Outlook: The Cost of Home Bias

Of the many unique traits of private banking clients in the region, one of the most renowned is the tendency towards home bias, characterized by a high concentration of investments in familiar local names. While the yesteryears of loose monetary conditions and strong growth prospects enabled many to generate impressive returns, it was only a matter of time before the law of averages would come into play for diversification to pay off.

The same theory will apply to private banks themselves moving forward.

Those that are still excessively dependent on the Greater China client segment, especially out of Hong Kong, will take a hit-or-miss approach in a market that could prove even more challenging in 2022 due to the addition of zero-Covid restrictions throughout mainland China and rising geopolitical risks. Diversification to Singapore as well as onshore markets may not easily result in record-breaking asset acquisition but will help act as a cushion to offset uncertainty from the world’s second-largest economy.

See finews.asia’s 2021 AUM League Table below.

(click on the table to enlarge)