Finma vs. UBS: Revenge of the Bureaucrats

Swiss regulators are mounting a puzzling offensive against the very mega-bank they helped merge in the 2023 emergency. Finance Minister Karin Keller-Sutter is keeping her head down. Fortunately, the decisive battle over capital requirements will be fought in Parliament, writes finews.asia.

How many employees at Switzerland’s financial regulator Finma could successfully run a global bank? The answer likely hovers around zero.

The tragedy of modern bureaucracy is that those least equipped to manage a successful bank business are often the ones lecturing those who can.

Maximum Pain

One expression of this imbalance surfaced recently: As financial news service Bloomberg wrote early last week, the Swiss Federal Council is likely to propose extremely painful new capital requirements for UBS on June 6 (paywalled article).

The driving force behind the proposal is Switzerland’s financial regulator Finma, with support from the Swiss National Bank (SNB).

25 Billion Francs More in Capital

UBS subsidiaries would reportedly need to be backed by 100 percent equity at the parent level—up from around 60 percent today.

For UBS, this would translate into an additional capital requirement of around 25 billion Swiss francs, resulting in a total CET1 ratio of 19 percent.

Market Alarm Bells

Bloomberg’s reporting—whose main findings were confirmed by finews.com through its own sources—sent shockwaves through financial markets. UBS stock lost nearly five percent last week, bucking overall market trends.

The market’s response was both wise and misguided.

Years of Lean Returns Ahead?

Wise, because investors understood just how central the capital issue is to UBS’s future. Raising such additional capital would be a watershed moment for shareholders: several key international business lines could become unprofitable, and UBS’s status as a globally credible bank could be called into question.

At the same time, the markets were misguided in exposing their lack of understanding of how Switzerland’s political process actually works.

Wrong Arena

In reality, the proposed rules—if they advance at all—won’t reach Parliament until next year at the earliest. And once they do, the debate will shift to a political arena where UBS is far more likely to prevail than in negotiations with Finma or the SNB. Those two bodies have been pushing their own dogma of «100 percent capital backing for subsidiaries» since Credit Suisse’s collapse—a uniquely Swiss obsession with no equivalent among other leading financial centers.

Yes, it can be argued—as Finma and the SNB do—that stronger capital buffers offer more protection in times of crisis. And it’s also true that Credit Suisse’s write-downs of its foreign subsidiaries contributed to its demise.

Targeting the Wrong Risk

But the Credit Suisse meltdown was not a capital failure—it was a liquidity crisis. In a confidence spiral where markets and depositors feed off each other, even a CET1 ratio of 19 percent may only delay the inevitable—and not necessarily prevent it.

It appears that regulators have fixated on a side issue and elevated it to the main threat, by virtue of their institutional authority.

Preferential Treatment for Credit Suisse

What makes Finma’s lobbying for this unprecedented tightening of capital rules particularly galling is the fact that this is the very same authority that granted Credit Suisse behind-the-scenes regulatory relief under the «Too Big To Fail» framework—via what became known as the «regulatory filter.» That practice began in 2017 and continued quarter after quarter, year after year—until the bank collapsed.

The parliamentary inquiry into Credit Suisse’s downfall noted that it was «unable to fully clarify the conditions» under which these filters were granted. Is Finma now punishing UBS for the sins it once helped enable?

Breaking Global Norms

This special treatment allowed Credit Suisse to report a CET1 capital ratio of 12.2 percent just four months before its demise. The real figure—without regulatory tricks—was closer to 6.9 percent. In the prior quarter, it had even dropped to 4.4 percent.

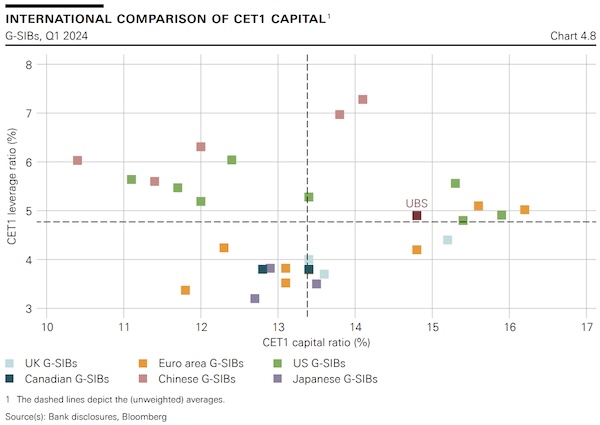

UBS, for its part, never used such «regulatory filters» and, according to the SNB’s own Financial Stability Report 2024, is among the best-capitalized Global Systemically Important Banks (G-SIBs) in the world.

Source: SNB, Financial Stability Report 2024

That Finma now wants to impose a 19 percent CET1 target on UBS—a figure that far exceeds global standards—is difficult to reconcile with the leniency once granted to Credit Suisse.

Should the proposal become law, UBS would be forced to choose: move its headquarters abroad or scale back into a Swiss retail bank with a reduced global wealth management arm.

Switzerland’s Anchor Institutions at Risk

Segments of corporate and investment banking would become unviable. That would also weaken Switzerland’s overall financial infrastructure, which is a critical location factor for the multinational firms that base their headquarters here. Not to mention: UBS contributes around 650 million francs in corporate taxes annually.

These arguments may fall on deaf ears at Finma and the SNB—but they could resonate more strongly in Parliament, or even with the Swiss electorate.

Next Milestone: June 6

The next chapter in the «Finma vs. UBS» saga likely unfolds on June 6, when the Federal Council is expected to present a framework for its so-called «Lex UBS.»

Finma’s position, supported by Finance Minister Karin Keller-Sutter, will likely shape the initial proposal. But with seven Federal Councillors and one Chancellor in the room, the outcome remains uncertain.

Costs Still Under Review

Additionally, the Federal Council is expected to present only the so-called «Eckwerte» (key parameters) for now, not fully drafted legislation. The sequencing seems premature: As finews.com has learned, the State Secretariat for International Finance (SIF) is currently tasked with conducting a so-called «regulatory impact assessment» of the proposal.

The results of this assessment will not be available until later and will be published alongside the official consultation documents. In other words, the Federal Council appears intent on setting key parameters before it even knows the economic cost of doing so.

Regulators Who Failed Seek Control

It bears repeating: Finma and the SNB failed in their oversight of Credit Suisse. Now, those same agencies are claiming authority over the future direction of UBS?

It takes little imagination to picture how persuasively government officials and regulators lobbied UBS Chairman Colm Kelleher and CEO Sergio Ermotti to take over Credit Suisse. And they did so despite having the means to resolve the crisis themselves.

Swiss Mediocrity as Default

The irony is bitter: the very bureaucratic caution—especially Swiss bureaucratic caution—that made UBS’s emergency acquisition possible is now turning against it.

Finma and the SNB no longer seem confident in their ability to supervise the banking giant they helped create. And tragically, they may not be entirely wrong. But instead of improving themselves, they want to trim UBS down to fit their own limitations.

Finma as Shadow Legislator?

Which raises the question: why hasn’t Finance Minister Karin Keller-Sutter stepped in to stop the regulatory machine? Quite the opposite—Finma Chairman Stefan Walter has been touring the country, actively promoting the plan his agency developed, as if he were an elected official.

One plausible explanation for Keller-Sutter’s reluctance is that the UBS situation, compounded by Finma’s power moves and looming state liability from AT1 lawsuits, may have simply overwhelmed her. Though she could have implemented the capital plan by decree, she chose to pass the hot potato to Parliament. Given her apparently shaky compass on financial-market matters, that may ultimately be for the best.

Favorable Odds for UBS

What will happen in Parliament? History shows that ideas born in regulatory backrooms are often improved, not worsened, by the political process. The right-wing SVP is firmly opposed. Even Keller-Sutter’s own center-right FDP is showing little enthusiasm.

Not a bad starting point, though the markets may see it differently on June 6th.