The 20-Year Bond in a Brave New World

The U.S. Government has responded to COVID-19 in unprecedented ways to produce a huge and rapid fiscal policy response. To fund this policy, the Treasury announced that it will issue over $800 billion in Treasury securities over the next three months. Including issuance completed in April, the issuance number rises to over $1 trillion.

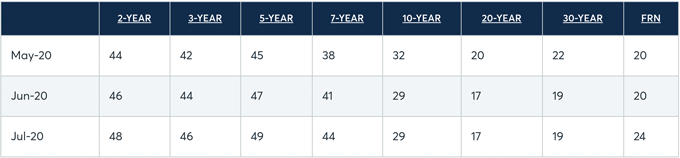

Treasury Issuance Details

In order to meet financing needs, the Treasury will issue a new tenor of 20-year bonds. Prior to the announcement, many market participants discussed the need to issue in a variety of other tenors including longer-dated 40- and 50-year securities.

For now, the addition of new 20-year security slots in neatly between the current issuance tenors of 10-year notes and 30-year bonds. The Treasury believes that there will be strong demand from investors for the 20-year bonds, which will allow the Treasury to finance its longer-term obligations at today’s very low-interest rates.

Changing Curve Dynamics

The 20-year tenor brings entirely new dynamics across the back-end of the curve, a segment that traditionally relied on old 30-year securities to provide yield guidance. The new bond will provide an additional trading point for both cash and derivatives products which have seen volumes surge in recent years. It is likely that this activity can increase; potentially dramatically.

According to Treasury data, on May 6, the 20-year yield jumped 9 basis points higher at the end of the day. Tellingly, the 2/20s curve steepened 7 basis points higher as the market digested this rates regime change. The market did not seem prepared for either the overall coupon issuance nor the size of the 20-year.

Gap in the Markets

At present, there is a two-decade gap between the issuance of a 30-year security and its next closest relative, the 10-year. This situation provides interesting dynamics for this large segment of the yield curve. As a 30-year bond ages, it generally becomes less liquid and more expensive to trade.

In order to reduce transaction costs, portfolio managers and other market participants generally prefer to infrequently trade securities in this region but to hedge them with more liquid parts of the curve. This can leave large duration mismatches and exposure without the proper tools to manage them.