How Banks Serve Multi-Segment Clients Best

There’s a transition going on within banks that operate in highly-populated Asian countries, where their customers’ personal wealth is growing at a fast pace.

Affluent customers in nations such as Thailand, Malaysia, and Indonesia represent high-net-worth assets, and banks in these countries must tackle the challenge of deploying modern solutions in order to address the financial needs of this new group of customers.

Bank advisors face the problem of how they best approach and serve their multi-segment clients in their home markets; often there is no one single advisory platform available that offers all the functionality required.

Therefore, banks that have customers that fall into the fast-growing «new wealth» category need to access a robust digital platform that is built on a solid infrastructure and can be deployed fast.

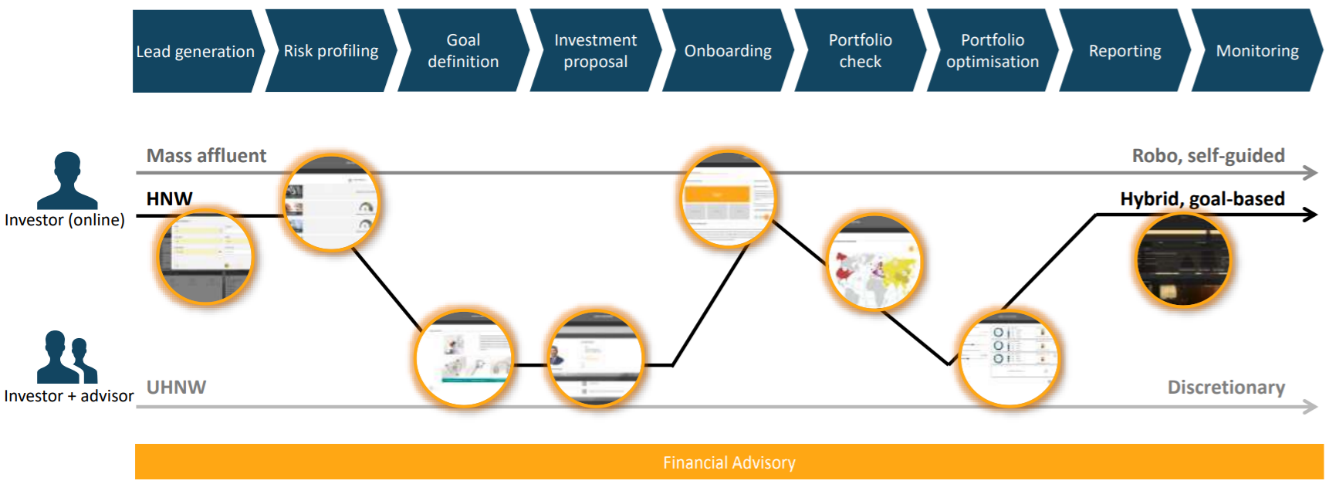

Digital Investment Advisory Services

Today, customers make use of the many available ways to find out about investment options and products and to compare offers. This means that the way customers and advisors interact is constantly changing.

A rising trend in recent years is the adoption of purely digital and hybrid investment advisory services by ultra-high-net-worth families in developing Asia as well as other markets. These customers, in particular, have high expectations and demand that their advisors are well-informed about their portfolio at all times.

According to global consultancy Accenture, an automated platform with periodic access to a human advisor ranks as the most preferred scenario across a range of investor profiles. Advisors with the right, pre-selected information can support their clients best and most efficiently.

(Source: CREALOGIX Digital Wealth Platform)

Build Versus Buy

When it comes to the question of whether a bank should choose a partner with an existing platform or build a solution themselves, the decision is influenced by many factors. Our checklist can help in this decision-making process. Demand for features and functionalities continues to increase, yet creating everything from scratch is time-consuming, and most often banks have no time to invest, especially if they want to stay competitive and play an important role in the battle for these «new wealth» customers.

If it’s a question of partnering with a third-party supplier, the bank must ensure it evaluates the platform, its capabilities as well as the ability of the supplier to deliver the solution within the required timeframe. The bank should talk to customers who have already deployed the solution and are running it.

And given the long shelf-life of software in financial institutions, the total lifecycle cost should be taken into account too. A stable FinTech company can offer a lot of know-how and expertise in managing such large projects and has experience in ensuring the seamless integration of third-party solutions via APIs.

360° Advisory Solutions

At present, banks are missing important sales opportunities when they cannot provide advice that is consistent and scalable. To respond to their customers’ needs, their advisors should be given access to a single platform to advise customers across multiple segments. A digital, out-of-the-box solution to improve the client on-boarding time facilitates objective-based consultations and allows advisors to serve clients end-to-end.

The CREALOGIX Group is a Swiss Fintech 100 company and is among the global market leaders in digital banking. We develop and implement innovative FinTech solutions for the digital bank of tomorrow. Banks can use our solutions to react to evolving customer needs in the area of digitalization, enabling them to hold their own in a very demanding and dynamic market and remain one step ahead of their competitors.

Founded in 1996, the group has around 800 employees worldwide. CREALOGIX Holding AG (CLXN)’s shares are traded on the SIX Swiss Exchange.

The CREALOGIX Digital Banking Hub relies on an API-based architecture: third-party systems and applications can be integrated easily via interfaces; the integration of software into partner applications is just as easy. The open API architecture meets the highest security standards and complies with all applicable regulations. Multi-banking modules give financial institutions considerable freedom; they can take on the role of account and data aggregator and sell their financial products through partner banks, fintechs, and technology companies outside the sector.