Vontobel's Financial Markets Outlook for 2018

«We see globally synchronized growth, strength in corporate earnings and modest inflation as a continued driver for capital markets with Emerging Market assets likely the best performers,» Daniel Bruesch says.

By Daniel Bruesch, Head Vontobel Wealth Management Investment Office, based at Vontobel Headquarters in Zurich

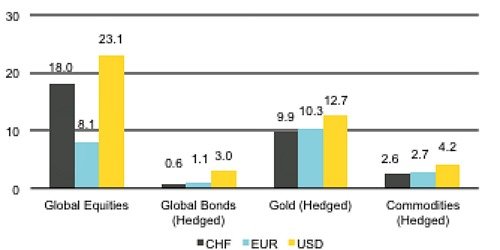

In 2017 investors enjoyed a stock rally that lifted the MSCI World, the U.S. stock exchanges, the Swiss Performance Index (SPI) and the German stock index DAX to new all-time highs and the Nikkei 225 to a 25-year high. By the end of the year, they had recorded a double-digit increase. Emerging market equity markets gained 31 percent in local currency terms.

The global investment grade bond markets recorded a modest increase (currency hedged) globally. Generally, corporate bonds yielded better than government bonds. Commodity markets closed 4 percent higher (in dollars) thanks to a good second half of the year. Gold rose by 13 percent (in dollars). The currency markets were characterized by the strength of the euro against the main currencies.

Financial Markets: Total Returns in 2017

Global Equities: MSCI World (Total Return); Global Bonds (Hedged): Barclays Global Aggregate Bond Index (Hedged); Gold (Hedged): Gold $/Troy Ounce (Hedged for CHF & EUR); Commodities (Hedged): Bloomberg 3-Month Forward Commodity Index (Hedged for CHF & EUR) Source: Thomson Reuters Datastream

Federal Reserve With Further Rate Hikes

The first year of the new US president Donald Trump ended with mixed results. He began the year with full-bodied promises for a trillion on infrastructure, tax cuts and less regulation. An initial Trump rally, however, petered out in the first half of the year, when numerous difficulties faced by the administration wiped out hopes of imminent economic stimulus.

Shortly, before the end of 2017 however, Trump achieved his first legislative success with the adoption of a sweeping tax reform (significant tax cuts for companies and easing repatriation of assets back to the US) that further boosted the U.S. stock markets which were also unphased by a change in guard at the Federal Reserve (Fed) and which raised interest rates three times in 2017.

Starting in February 2018, Jerome Powell, the new head of the Fed, will continue to lead the world's most important central bank and has already signalled that the cautious course of normalizing monetary policy of the outgoing Fed chief Janet Yellen will be continued.

Relief in Europe

The election of the new French president Emmanuel Macron was received with relief in Europe and gave the euro a boost. More importantly, the old continent recorded the strongest economic growth in a decade, outpacing even the United States. It is important to note that economic momentum has been strong in the Eurozone as a whole, including the periphery.

In an early parliamentary election, Japan confirmed a fourth term of office for Prime Minister Shinzo Abe. Abe's reforms, coupled with loose monetary policy, are increasingly bearing fruit. In the third quarter, the Japanese economy grew for the seventh consecutive quarter, the longest period since the beginning of 2001.

In the emerging markets, China was an important driver, with growth of 6.9 percent in the first half of the year and 6.8 percent in the third quarter. Production is robust, domestic consumption is strong and exports are recovering. India also gained traction in economic growth, up 6.3 percent in the third quarter. The economy appears to have overcome the slowdown resulting from the monetary reforms of November 2016.

Outlook 2018

Our main scenario for 2018 is a continuation of the «Goldilocks» environment. By this we mean that the global synchronous upswing will continue without inflation accelerating too much and that asset prices will remain elevated.

We expect the U.S. economy to grow by 2.5 percent. Tax reform could provide an additional impetus of 0.8 percentage points. However, the U.S. economy is almost fully utilized and tax reform will add to the burden of the twin deficits. As far as foreign trade and immigration are concerned, we expect the status quo to continue: the North American Free Trade Association (NAFTA) will continue to exist, while the relationship of the U.S. with China will remain intact. We are encouraged by the planned deregulation of the banking sector.

On a Solid Growth Course

We see Japan and the Eurozone on a solid growth course, but slightly weaker than in 2017. Supported by the global economic upturn, the Eurozone will be able to maintain its growth momentum in the coming year. The still extremely favorable sentiment indicators point to a continued strong start to the new year.

However, a renewed acceleration of growth is not expected in our main scenario, as the euro area is about to close the output gap next year and the strength of the euro is increasingly an issue for corporate earnings. Political events - such as elections in Italy, the political stalemate in Germany and negotiations between the U.K. and the EU are further potential risks. Unemployment in the Eurozone continues to decline, without this leading to significantly higher wage growth. Core inflation is therefore likely to increase only slowly. Under these circumstances, we see the ECB continuing its liquidity measures as planned with monthly bond purchases of 30 billion euros until the end of the third quarter of 2018, then phasing them out and stopping them by the end of the year. In our main scenario, we do not forecast an increase in key interest rates in 2018.

China in a Controlled Manner

In Japan, we expect Prime Minister Shinzo Abe to continue his economic program known as «Abenomics». With the likely reappointment of Haruhiko Kuroda as governor of the Japanese central bank (BoJ), monetary policy is likely to remain virtually unchanged at least until mid-2018. This means a weak yen for the time being which will substantially support exports. Structural reforms, consumer led growth and positive earnings momentum are at the core of our conviction for Japanese equities.

We assume that the Chinese economy will weaken slightly, in a controlled manner in 2018. However, growth in other emerging markets can more than compensate for this. We see stronger growth momentum particularly in Brazil, Russia and India. Inflationary pressures are also likely to gradually increase in the emerging markets and lead to isolated interest rate hikes.