CME: QE Link to Gold, Silver and Tech Stocks?

Central banks injected unprecedented levels of liquidity into the banking system and bond market amid pandemic-related shutdowns of large segments of the global economy.

By Erik Norland, Executive Director and Senior Economist, CME Group

As a result, the balance sheets of the Bank of Japan, Bank of England, Bank of Canada, European Central Bank and the U.S. Federal Reserve (Fed) are at their largest levels when measured relative to their respective GDP (Figure 1).

Figure 1: Central bank balance sheets expanded to record size, but the pace of growth slowed in Q3.

Most of the expansion took place between March and June, and the asset purchases have slowed significantly since, especially in the U.S. The Fed expanded its balance sheet by $3 trillion between mid-March and mid-June but has since stated that it will slow further asset purchases to around $25 billion per month – which may sound like a lot but it’s a 97.5 percent decrease from the March-to-May pace of growth (Figure 2).

Figure 2: The pace of expansion slowed over the summer especially in the US (in light blue).

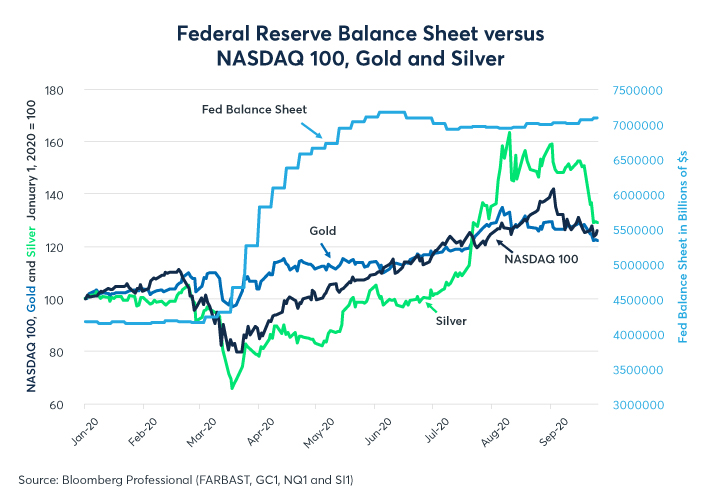

It’s too early to say if the balance sheet expansion will have any impact on consumer prices, but if the past decade’s experience with quantitative easing (QE) is any indication, the impact on consumer prices may turn out to be minimal. Asset prices are another story. The prices of certain types of assets responded strongly to the increase in the amount of central-bank credit, notably the price of gold, silver and technology stocks, like those that dominate the Nasdaq 100 index.

- The Nasdaq 100 rallied 88 percent from its March lows to its high in early September.

- Silver rose 157 percent between mid-March and early August.

- Gold rallied 42 percent off its March lows, also peaking in early August.

Since then, all three markets have moved lower. By late September gold had fallen 10.5 percent from its highs, the Nasdaq 100 has fallen by 14 percent, and silver is down by 26 percent (Figure 3). It is possible that these declines are merely corrections after such powerful rallies.

Figure 3: Did the balance sheet expansion cause the rally in gold, silver and Nasdaq 100?

There is, however, another possibility: all three markets may have been propelled by the Fed’s balance sheet expansion and have since lost steam as the Fed, and to a lesser extent its peers, slowed the pace of QE. Two factors point in the direction of this possibility:

Erik Norland is Executive Director and Senior Economist of CME Group. He is responsible for generating economic analysis on global financial markets by identifying emerging trends, evaluating economic factors and forecasting their impact on CME Group and the company’s business strategy, and upon those who trade in its various markets. He is also one of CME Group’s spokespeople on global economic, financial and geopolitical conditions.