The year starts with a significant rally, but it could be so much more if people knew how and what to invest in.

The mainland’s equity markets, and with that, Hong Kong, are up sharply this year, with the flow of inbound buy orders being roughly three and four times that of sell orders.

Foreign institutional investors seem to be returning to the market on the back of the surprisingly sudden relaxation of the government’s zero-Covid policy.

The thing is – it could all be so much more.

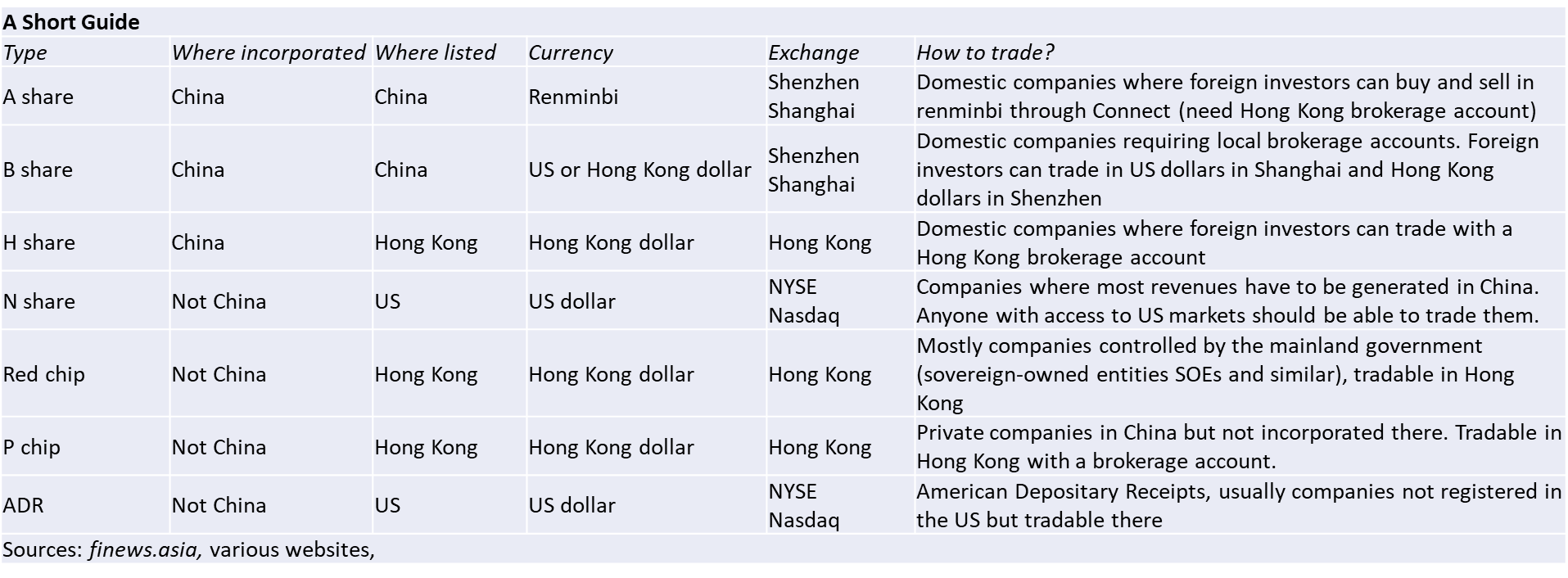

Between A and B

In reality, the interest of the average overseas investor is likely to wane at the first mention of the differences between A and B shares, the mechanics of North and South-bound Connect schemes, and the necessity of opening a far-off, long-distance brokerage account (refer to guide below).

Even sophisticated family offices without specific country expertise on hand are liable to get waylaid by the liberal use of the Latin Alphabet by the time H or N comes along.

After being introduced to red chips and P chips and around the time they get to a somewhat familiar term – ADRs – it is not altogether surprising if they have internally made up their minds to delegate any investment into the mainland’s markets through the secondary vehicles on offer at various private banks.

Onshore and Offshore

MSCI researcher Wei Xu confirmed in a note last week that integrating onshore and offshore mainland-based equities would go a long way towards ameliorating that conundrum while offering investors a more diversified exposure to China’s economy.

As part of that, he noted the noticeable dispersion in returns between MSCI China-related indexes, saying that the segmented approach with different listing locations has prompted a plethora of share types.

They also face different risks, with P chips and overseas listings, naturally, being more exposed to the regulatory pressures in China and delisting risks from US auditing requirements, something finews.asia has discussed extensively.

Integrated Offering

Xu pointed out that the locally based A-share market is more diverse, larger, and less concentrated than all the offshore markets, with the market cap of the latter being less than half of the former, and it has the potential to be «more balanced and resilient» in downturns.

Another A-share market expert at a Hong Kong-based trading specialist told finews.asia that the equity universe in China was so large, diverse – and segmented – that it could be diced up in several different ways, each of which could get investors to arrive at different conclusions.

«Investors need to realize that Chinese equities, like the economy, are not homogenous entities. It is an extremely diversified market with tremendous idiosyncratic risks - and opportunities,» the expert maintained.

Range of Performance

He added that it can be looked at from the perspective of share class, market capitalization and sector. All can show a wide range of performance over a variety of given periods, the expert indicated.

But there is also another missing in all of this. Easier access for international retail investors. Although that discussion is still likely premature and involves further steps to liberalize the market and a fully convertible, free-floating currency, the ultimate goal should be to add China to the list of standard markets in significant online brokerages (Swissquote provided as example).

That would likely pave the way for far greater acceptance and knowledge of China’s markets, including with high-net-worth clients overseas.