Ernst Fehr, a professor of economics in Zurich, has developed a new methodology to evaluate the performance of the management of a company – regardless of the share price. Adriano B. Lucatelli, an expert in finance, has calcualted the new indicator for Swiss companies and is presenting the results in an exclusive essay to readers of finews.first.

Good management in general has a beneficial impact on the valuation of a company. But often, it is difficult to construct a direct link to the share price. Factors of coincidence frequently affect the performance. Or as a saying has it: «A rising tide will lift all boats, including the ones with holes in their hulls.»

A new evaluation methodology by Ernst Fehr of Fehr Advice, a Zurich-based consultancy, evades the problem and sheds light on the issue. Surprises can't be excluded.

«The aim is to see how well and how quickly the management is able to row»

Based on total shareholder return (capital gains and dividends), coincidental factors of the market are eliminated and the «Market-Adjusted Performance Indicator» (MAPI) is determined. With the aim to take the wind out of the sails of the boat and to see how well and how quickly the management is able to row.

MAPI is calculated via correlations and covariances on the basis of a worldwide pool of companies. This produces a company-specific index, which can be compared with the total-shareholder-return of the company in question.

The weight of the companies included in the index is based on the level of correlation with the market the evaluated company is active in. The higher the correlation, the bigger the weight in the MAPI.

Instead of matching the performance in the market with a stock index, every company is compared with a clone with very similar risks. The management has done well if the MAPI is above zero; if the MAPI is negative, the expectations haven't been met.

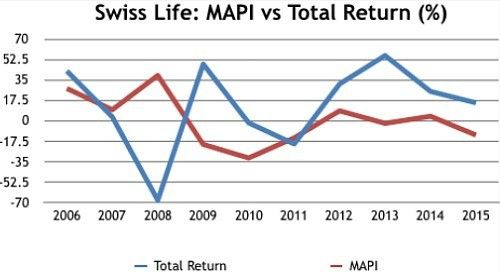

«Swiss Life destroyed several billion Swiss francs in shareholder value»

It is little surprising that most companies listed on the Swiss Performance Index (SPI) had a decent performance. Only a few sectors, such as biotech, outperformed over the past decade.

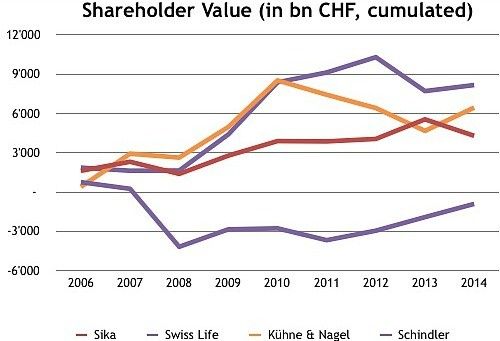

The results of the individual companies produce some unexpected patterns (illustration below).

(Sources: Thompson Reuters and own calculations)

The insurer Swiss Life for example destroyed several billion Swiss francs in shareholder value (illustration below). No surprise then that the stock price of Swiss Life substantially underperformed compared with the SPI since the company's listing on July 3, 1997.

The main reason for this lies in the wrong legal form of the company. The major part of the company's surplus is being handed out to customers via guaranteed payments instead of to shareholders. The insurance takers each year benefited from their guarantees and surplus payments, while shareholders repeatedly were asked to open their purses in capital increases and had their dividends cancelled.

It would be wrong to blame this result on the management alone though. The MAPI mostly was in positive territory. Thus, it becomes apparent that the management did a good job even though for systemic and structural reasons the share price developed moderately only.

In cases of investors or groups, where families, trusts or employees exerted power over the company, producing a value for shareholders was mostly in the plus.

Such investors on average take a long-term view and aren't prone to changing strategies because short-term and temporary fluctuations. The conflicts of interest between owners and management at those companies is furthermore less pronounced.

«Mistaken restraint»

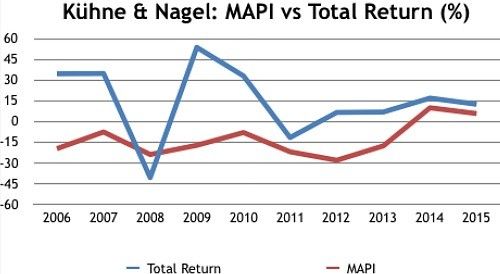

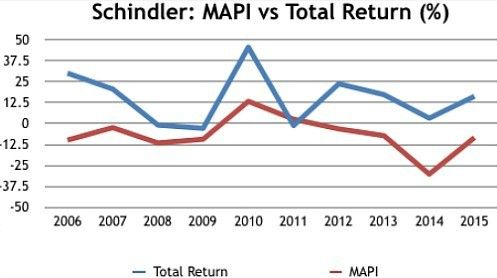

The strong increase in value at some family companies isn't the result of exceptional performances of the management though. It seems that the main shareholders refrain from asking the management to exhaust the profit potential of the company.

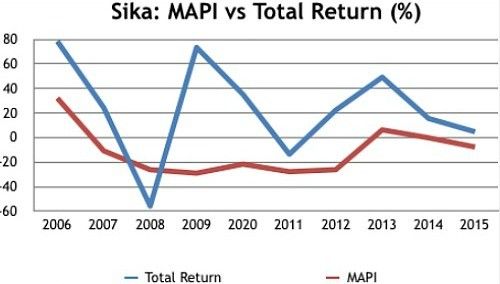

Examples of this are Kuehne & Nagel, the logistics company, Schindler (elevators) and Sika (construction chemicals). The performance of the management remained below the potential for years, while shareholder value increased substantially (illustrations below).

The restrained approach of owners can be viewed and approved of as a contrast to the «unfettered» pursuit of shareholder value. However, not to exploit the profit potential to put money aside out of mistaken restraint will come back to haunt the owners earlier or later.

It is worth checking out the MAPI of high achievers on the stock market. Good total shareholder return figures tend to gloss over mediocre management performances. In those cases, shareholders can ask for more from the company leaders.

Inversely is a negative shareholder value such as the one of Swiss Life not always is a sign of bad management. The MAPI supports shareholders to make a fair judgement of the management and in exploiting the full profit potential. A transparent compensation policy is an important precondition to reach those two goals.

Adriano B. Lucatelli, a 50-year-old Swiss, is a senior lecturer at the University of Zurich, chairman of the readers' commission of Neue Zuercher Zeitung and entrepreneur in the financial services industry. He is also co-founder of Vormaerz, a think tank promoting the dialogue between companies and the financial market. Lucatelli studied international affairs and economics at the University of Nevada, Reno and at the London School of Economics. In 1995 he obtained a PhD from the University of Zurich with a dissertation on global financial market regulation.

He is co-founder and managing director of Descartes Financ. He started his professional career at Credit Suisse in 1994. From 2002 to 2009, Lucatelli was managing director at UBS Switzerland and member of the management committee in Lugano and Zurich.