T. Rowe Price: Asset Management – a Journey Through Time

Asset manager T. Rowe Price has opened its archives for finews.asia. A closer look at the historical documents reveals a new perspective on the history of asset management. Here is part two.

In part one of this series, we have taken a closer look at how the financial industry developed during and after the Great Depression. Before 1940, the asset management branch was quite unstructured and some players operated in grey areas.

Yet, in 1940 regulations were put in place that aided in bringing some order into a formerly rather non-transparent sector. Now it is time to move on and take a look at the flourishing industry in the 1950s and 1960s.

The 1950s and 1960s were considered the booming years of the U.S. economy. The United States was the world’s strongest military power. Its economy was booming, and the fruits of this prosperity – new cars, suburban houses, and other consumer goods – were available to more people than ever before. While the 1950s were also an era of great conflict, unemployment rates were low. New jobs were created in a thriving manufacturing and construction sector.

Small Asset Management Firm Grows

(Thomas Rowe Price, 1898-1983)

The year 1950 was also the first profitable year for a small asset management corporation in Baltimore which had been funded in 1937 – T. Rowe Price. In comparison to other asset managers at that time, T. Rowe Price acted very solidly and with high moral standards. Because of this belief, his corporation progressed much slower than competitors.

At the same time, the firm was also able to withstand financial turmoil much better than a lot of its competitors.

Four Employees

However, as the economy was improving fast after 1950, T. Rowe Price was able to increase the number of its clients within the next decade. In 1951, T. Rowe Price was, therefore, able to sign its first institutional client. The first mutual fund was introduced to the market in 1950.

While the corporation had four employees in the 1940s, in the 1950s the number of employees rose to 15 people. To keep up with a surge in clientele, T. Rowe Price hired an unprecedented new cohort of research analysts and relationship managers in the early 1960s, many of whom stayed with the company well into the 1990s.

Modern Portfolio Theory

In 1952 the «Modern Portfolio Theory» was developed by Harry Markowitz. The focus of this theory is diversification.

«Markowitz was the first to formalize the measurement of portfolio risk and return in a mathematically consistent framework, which he subsequently expanded. Acknowledging that measuring portfolio risk and portfolio return was only the first step, Markowitz introduced a methodology for assembling portfolios that consider the expected returns and risk characteristics of the underlying assets as well as the investor’s appetite for risk. The result, usually referred to as the modern portfolio theory, pushed portfolio construction toward a science and away from being an art», explains François-Serge Lhabitant in his scientific analysis.

For their theory, he and his associates William Sharpe and Merton Miller were awarded the Nobel Prize in Economic Science in 1990.

(Harry Markowitz on the occasion of the presentation of the Nobel Prize)

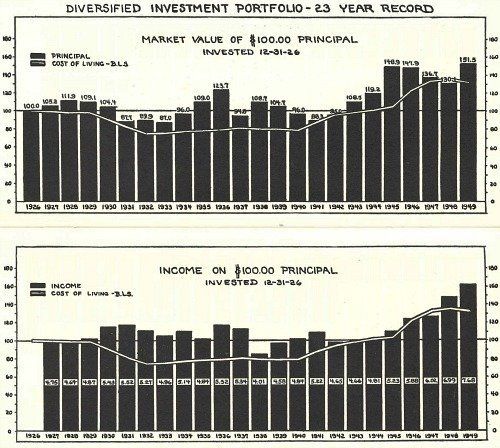

Diversification is now used by analysists of asset management corporations to achieve the best amount of return for a certain level of risk. Risk is hereby defined as return volatility. While some asset managers underwent an evolution of their processes, others, such as T. Rowe Price or J.P. Morgan Chase still adhere to the theory and use diversification as their main tool of financial management.

Additionally, in the middle of the 1930s, Thomas Rowe Price developed his «Growth Stock Theory». A growth stock is defined as a «stock of a corporation that has faster than average gains in earnings and is expected to continue to» keep up the speed. This theory made Price famous and well known throughout the entire industry, explains Emily Davidson, archivist at T. Rowe Price.

International Expansion, Not Yet

Between 1950 and 1960, T. Rowe Price grew even larger, still slower though than competitors such as Alex Brown or J.P. Morgan Chase. But that was intended by the asset managers leadership. The firm's focus was on long-term gains instead of short-term profit. By 1960 the decision was made to hire more people. In the same year, the second fund was introduced to the market, ten years after the first.

While the firm had a small office with five employees in New York City, headquarters remained in Baltimore. T. Rowe Price’s management did not yet see a need to expand further. It would take T. Rowe Price another decade before the Baltimore corporation would establish a basis for international operations.

(In 1950, Thomas Price explains his investment strategy and research process)

But this is not the end of this exciting story. In the next part of this series, we look at the expansion from the U.S. to Europe. How did asset management grow with regard to AUM numbers? And how was the development influenced by events in the financial world? Stay tuned!

With material provided by Emily Davidson

This material is being furnished for general informational purposes only. The material does not constitute or undertake to give advice of any nature, including fiduciary investment advice, and prospective investors are recommended to seek independent legal, financial and tax advice before making any investment decision. T. Rowe Price group of companies including T. Rowe Price Associates, Inc. and/or its affiliates receive revenue from T. Rowe Price investment products and services. Past performance is not a reliable indicator of future performance. The value of an investment and any income from it can go down as well as up. Investors may get back less than the amount invested. The material does not constitute a distribution, an offer, an invitation, a personal or general recommendation or solicitation to sell or buy any securities in any jurisdiction or to conduct any particular investment activity. The material has not been reviewed by any regulatory authority in any jurisdiction. Information and opinions presented have been obtained or derived from sources believed to be reliable and current; however, we cannot guarantee the sources' accuracy or completeness. There is no guarantee that any forecasts made will come to pass. The views contained herein are as of the date noted on the material and are subject to change without notice; these views may differ from those of other T. Rowe Price group companies and/or associates. Under no circumstances should the material, in whole or in part, be copied or redistributed without consent from T. Rowe Price. The material is not intended for use by persons in jurisdictions which prohibit or restrict the distribution of the material and in certain countries the material is provided upon specific request. It is not intended for distribution to retail investors in any jurisdiction. © 2019 T Rowe Price. All rights reserved. T. ROWE PRICE, INVEST WITH CONFIDENCE and the Bighorn Sheep design are, collectively and/or apart, trademarks or registered trademarks of T. Rowe Price Group, Inc. 201904-82293