Will the Year of the Earth Pig Bring Fortune and Luck?

Concerns about China abound, including a build-up of debt, negative demographic trends, state-owned enterprise inefficiency and general corporate governance risk. These are the challenges. Yet, we should not ignore China’s ongoing transformation.

By Wenchang Ma and Greg Kuhnert, Portfolio Managers at Investec

China's transformation addresses many of the concerns investors have and supports the development of the equity market over the long term.

Government reform efforts are happening on multiple fronts. Supply-side reform has nearly completed its third year, with capacity reduction targets well on track and even exceeding expectations in certain industries such as steel. Environmental control remains stringent, driving significant decreases in air and water pollution.

State-owned enterprise reform is helping to align the interests of the state, management teams and public shareholders. Financial reforms continue to foster better risk control in financial institutions and a further opening of the domestic capital market to global investors.

Increasing Demand for Higher Quality Products

With a large consumer base and growing wealth, China has seen increasing demand for higher quality products and services. Large numbers of Chinese go on shopping sprees abroad, which is driving domestic companies to innovate so that they can capture more market share. Good infrastructure and efficient supply chains provide the backbone for a more innovative China. An abundant and inexpensive talent pool, significant social capital and supportive government policy also play crucial roles.

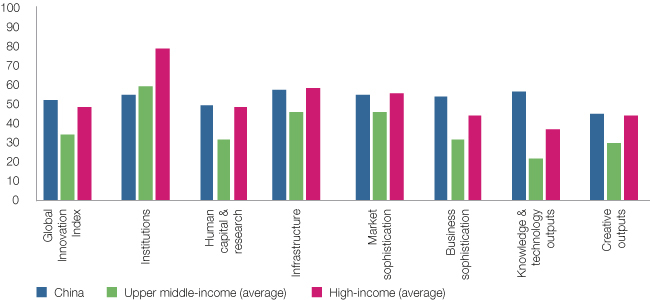

An example of this is the World Intellectual Property Organisation’s Seven Pillars of Innovation, where China has generally performed in line or even better than the average high-income country, and is well ahead of what might be a more obvious comparator, the average for upper middle-income countries.

The Seven Pillars of Innvation

Although more and more investors, both institutional and retail, are considering strategic allocations to China, they remain underweight despite moves to open capital markets and make investing in China easier.

Faster Than Expected

MSCI is looking to quadruple China A-share weighting in its major benchmark indices from 2019, only one year after its initial inclusion, which is faster than the market expected. FTSE Russell will also start phased inclusion from June 2019, which will see China A-shares representing 5.5 percent of its emerging market index.

If fully included, China A-shares should account for more than 16 percent of the MSCI Emerging Markets Index and more than 20 percent of the Russell Emerging Markets Index. China’s onshore and offshore markets together will account for over 40 percent and 50 percent of the two indices, respectively.

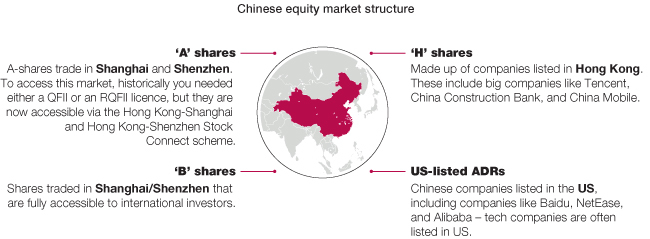

Chinese Equity Market Structur

Given China’s strategic importance, attractive long-term growth potential, increasing index inclusion and diversification benefits, we think global investors’ allocation to the world’s second-largest equity market will grow over time. Increasing foreign investors’ participation should help reduce market volatility and improve pricing discovery in the A-share market.

Drawdown offers potential entry point

Following a significant pullback in 2018, the Chinese equity market currently trades below its 10-year historical average valuation level from both the forward price-earnings and the price-to-book perspective. The valuation discount versus developed markets has widened despite the more positive growth outlook.

Stock selection opportunities and risks

Growing Trade Tensions

Although we do not attempt to call the bottom without seeing evidence of positive surprises on corporate earnings, an increasing number of opportunities are emerging on the back of the market pullback. As more value emerges, we are finding opportunities in a number of sectors. The evidence suggests that companies with good quality, attractive valuations, improving operating momentum and increasing investor attention tend to outperform over the long term and this remains the framework for our stock selection. Our 4Factor screen currently sees most opportunities in the materials, energy, financial, utility, and communication services sectors.

Clearly, the Chinese equity market faces short- to medium-term, most significantly policy execution and growing trade tensions between China and its trade partners, particularly the US. Over the long term, we believe a consistent investment strategy focusing on identifying high conviction ideas, using a bottom-up approach, is the best way to provide long-term risk-adjusted returns to our investors. We remain broadly fully invested in our portfolio as there are abundant opportunities that can be found in a dynamic market environment such as China.

- Read an extended version of this article here.