Credit Suisse has had its first loss in the first three months of the year since 2009 – yet the shares are rising. Nine thoughts about today's release.

1. Giving Priority to Private Banking Was Long Overdue

Credit Suisse CEO Tidjane Thiam suffered his personal Waterloo during the first quarter of 2016. He was heavily criticized internally and externally on the basis of the massive write-down in investment banking. Simultaneously, it became evident that his switch towards giving priority to private banking had been long overdue.

The two investment-banking units had losses while private banking and the regions posted profits. The problems at the investment banking was sufficient to drag the bank into loss-making territory even though only a third of the group's revenue is being generated by the two investment-banking units.

- Conclusion: of course, investment banking is cyclical by nature. But surely, the first quarter has proven that the former pride of Credit Suisse (CS), the investment-banking arm, has to be cut down to size or even face being sold.

2. Global Markets: Elimination of Risks

The two portfolios of distressed debt and collateralized loan obligations (CLO) have turned into a nightmare for the CS leadership. The bank had to write down a billion Swiss francs. And the problems also caused an almighty row within the bank and a revolt by the New York-based investment bankers (assisted prominently by the «Wall Street Journal» against CEO Thiam.

The top executive at CS had ordered the elimination of the risky positions as quickly as possible. The bank acted radically and without taking care about the whims of the market. The CLO positions have been reduced by 81 percent compared with the fourth quarter and 79 percent of the distressed debt were also removed – with TSSP assuming 1.27 billion francs.

- Conclusion: following this clean-up, the potential loss at Global Markets in a situation of stress should only reach half the level of what it has been so far. Of course, further losses are still possible, not least because the market for these products is challenging.

3. Wooing the Shareholders

CS is still less well capitalized than the average bank of its size. Thiam still has a lot to do in this respect. Little surprise then that shareholders are awarded a bonus. They get a discount for buying shares. The management has taken on board that it needs its shareholders to succeed.

- Conclusion: the bank's equity securities rose 5 percent after the publication of the quarterly report this morning. It is early days still, but a sign it was that the stock may recover some of the lost ground.

4. Cost-Cuts Paving the Way

CS will only make it if it intensifies its cost-cutting measures. The plan to cut 6,000 jobs by year-end seems on course, with 3,500 already eliminated.

Investment bankers are affected by the cull, but also client adviser in private banking inside and outside of Switzerland (see pages 21 and 22 of today's release). Asia Pacific is the only segment to significantly expand the number of client advisers as Francesco de Ferrari told finews.ch earlier this year.

- Conclusion: many CS employees still face a difficult time at their workplace. The tension will probably be part of their life for at least another year.

5. Transition at Swiss Universal Bank

The Swiss Universal Bank under the guidance of Thomas Gottstein will start afresh in the second half of the year and expects to go public in the first half of 2017. With the proceeds of the IPO CS wants to improve the capital base. The IPO will of course depend on the market conditions, the bank stressed today.

The change of the Swiss unit into a so-called entrepreneur's bank has left its marks on the number of employees. The Universal Bank had 1,560 client advisers at the end of March, compared with 1,600 a year earlier. The unit improved both pretax profit and net new money.

- Conclusion: 2017 will be the year when the Swiss Universal Bank will be scrutinized more thoroughly. And that's when it will be decided how the bank will look in future.

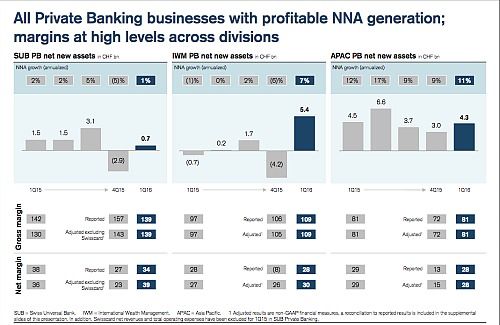

6. CS Is Attracting Money Again

At the end of 2015, the bank was leaking client assets, bot at the Swiss Universal Bank as well as at International Wealth Management. The trend has been reversed and the Zurich-based bank recorded net new assets amounting to 10.5 billion francs in the first three months of the year. Iqbal Khan's International Wealth Management took the lion's share with 5.4 billion (see table below).

- Conclusion: margins and net new assets are both improving. The business with Asian clients was particularly profitable.

7. Oil and Gas Loans Remain a Worry

CS in the first quarter increased the amount of loans to the oil and gas sector by $200 million to $9.3 billion compared with the fourth quarter. Most of the increase is attributable to North America with 38 percent not fulfilling the «investment grade» status.

Loans to oil-producing companies amount to $3.3 billion. The oil price has recovered to $44 from a low of $27 in January. Still, this isn't enough for the U.S. producers because of their more expensive technics used to extract the oil.

- Conclusion: the future of the oil price will heavily influence the balance sheet of CS.

8. Optimism Is Back

In October 2015, Credit Suisse presented a set of pretty optimistic goals. Many experts doubted that the goals were attainable given the increased regulation and because of difficult market conditions.

Thiam remains optimistic and says that the banks remains focused on achieving its goals regarding cost cuts and on investment in profitable growth and capital management.

CS has said it wants to increase pretax in Asia Pacific from 400 million last year to 2.1 billion by 2018. In International Wealth Management the projection is for a pretax of 2.1 billion compared with 0.7 billion in 2015. And the Swiss Universal Bank will have to contribute with 2.3 billion to the group's pretax by 2018, up 600 million from 2015.

- Conclusion: way to go.

9. CS' Capital Base

CS has less capital to rely upon than UBS and hasn't improved quarter-on-quarter. The core capital ratio is 11.4 percent (UBS: 14 percent), the leverage ratio is 3.3 percent (UBS: 5.4 percent). CS has to return to profit to improve those statistics. Shareholders would hardly accept a further capital increase.

- Conclusion: capital remains low and will remain so for quite a while.